Central Bank Outlook Is The Path To Success

Policy Tightening Is On The Way

The March round of central bank meetings has come and gone. The results are largely as expected with the usual changes in nuance to drive analysts crazy. While most banks see economic growth accelerating and the need for tighter monetary policy their newly minted hawkish positions are tempered by low inflation. No central bank, not the FOMC the BoE the BOJ or BoE see inflation rising at a rate fast enough or to a level high enough for them to raise their long term forecasts.

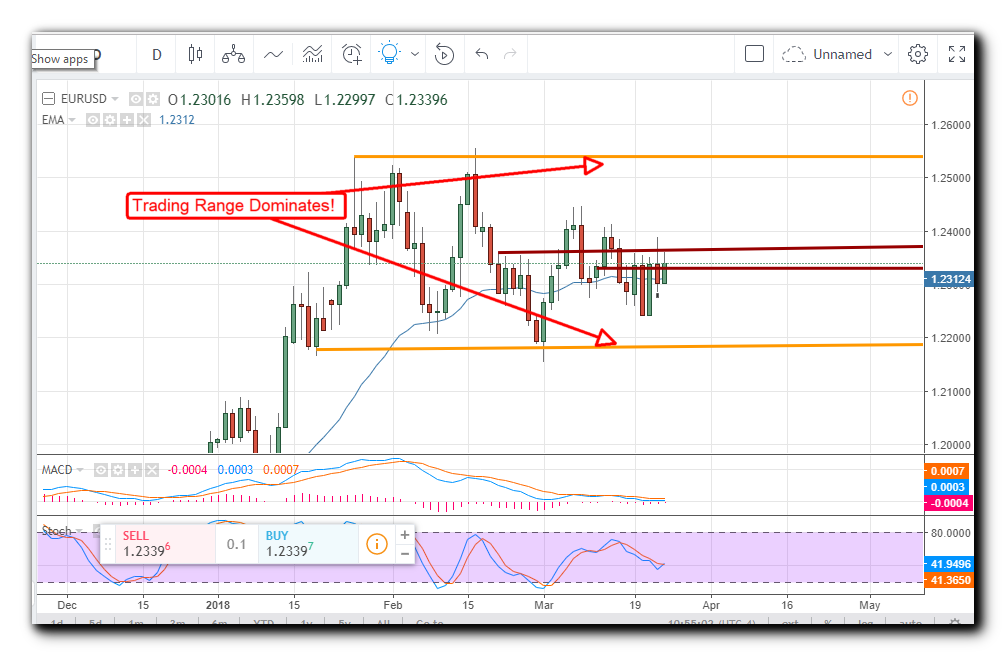

What this means for traders is simple. Recent trading ranges, ranges dominated by central bank expectations, will continue to dominate the market over the near term and perhaps longer. This means support and resistance targets are likely to produce price reversals and should be watched closely for entry and exit signals. Looking forward economic data will drive prices as it leads the market in one direction or another, up to and until the next round of central bank meetings.

The Spring 2018 Central Bank Outlook

The Bank of England – The BoE just released their latest policy statement and held rates unchanged. The vote was 7 to 2 in favor of a hike showing a split in opinion that foreshadowed their rate hike last fall. Traders now expect with a near 100% certainty the bank will raise rates at the May meeting scheduled for Thursday the 10th. The bank also upped its forecasts for GDP as global markets are also rising; where one nation improves it now leads to improvement throughout the system and this will keep inflation on the rise. The market had been pricing in 2.5 hikes over the next 3 years, this raises the chance there will be at least 2 if not more and that will keep the pound firm.

The European Central Bank – The ECB just released their quarterly Economic Bulletin. The bank sees global economic growth accelerating above expectations and helping the EU economy do the same. While they did raise their global and EU GDP estimates, as well as expectations for policy tightening, they did not alter the inflation forecast for the long term. The news helped to firm the Euro but not enough for it to break out of its trading range versus the dollar. The next ECB meeting is scheduled for April 26th where they are not expected to alter policy. What they are expected to do is confirm the end of QE by indicating asset purchases will end in October as planned.

The Bank Of Japan – The Bank of Japan has been quietly improving the economy of Japan for the last few years and recently, to little fanfare, announced that QE could end soon. There is still little expectation it will happen this year but soon is a lot sooner than anyone was expecting. The bank says global growth has helped Japan reached sustainability, once they are comfortable with the trajectory of inflation they will begin to alter policy. The next BOJ meeting is scheduled for April 26th, the same day as the ECB, so volatility should be extreme to say the least.

The Federal Open Market Committee – The FOMC just raised rates by a quarter point to a range of 150 to 175 bps. This move is as expected, as was the intensified hawkishness displayed by new chief Jerome Powell. This news helped strengthen the dollar although the longer term outlook, that inflation was expected to remain low, kept those gains in check and the Dollar Index within its expected range. The next FOMC meeting is in June, June the 13th, and they are expected to raise rates again with an 80% probability.